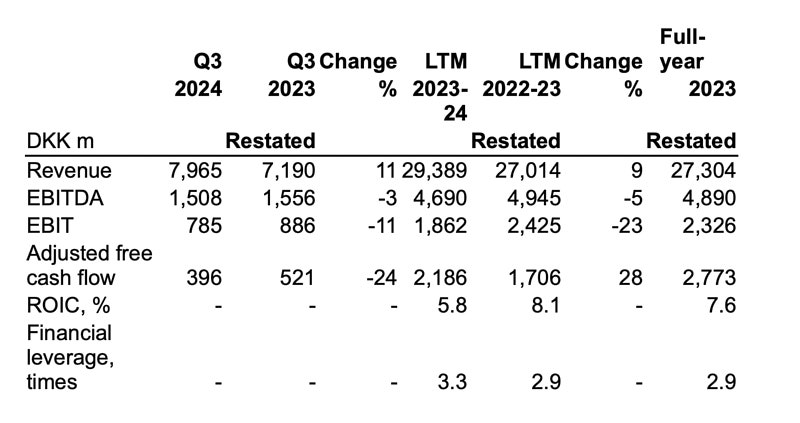

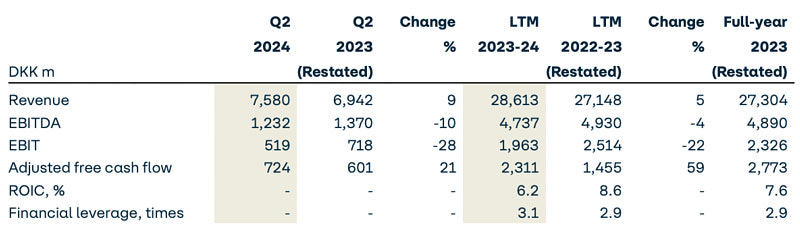

DFDS’ EBIT outlook range for 2024 is revised following results below expectations driven by mainly a more widespread slowdown in Europe than previously expected as well as intensified competition in northern European land transport markets and the Mediterranean freight ferry market.

The current market conditions are expected to continue for the rest of the year whilst a rebound in activity was previously expected for the rest of the year.

The termination of the share purchase agreement to acquire the international transport network of EKOL Logistics may moreover in Q4 2024 entail some financial impact.

As a consequence, the EBIT 2024 outlook range is lowered to DKK 1.5-1.7bn from previously DKK 1.7-2.1bn, and the outlook for the adjusted free cash flow is changed to around DKK 1.2bn from previously around DKK 1.5bn.

The revenue growth 2024 outlook is changed to 8-10% from previously 8-11% as revenue from EKOL Logistics was previously included in the revenue outlook.