According to the latest data of the Hellenic Statistical Authority (ELSTAT):

+19.2% total passenger traffic

+3.3% total traffic of mobile units

According to the latest data of the Hellenic Statistical Authority (ELSTAT):

+19.2% total passenger traffic

+3.3% total traffic of mobile units

According to Anek Lines’ latest report on the 9-month and 3rd quarter key financial results that was published on December 9, 2022:

For the nine-month period ended 30 September 2022:

Ferry operation EBITDA increased significantly compared to last year: SEK 4,189 (2,675) million.

The result is mainly an effect of increased travel and freight volumes as well as improved travel rates compared to last year.

EBITDA from chartering out ropax vessels increased by SEK 227 million to SEK 441 (214) million in the nine-month period ended 30 September 2022 mainly due to the delivery of CÔTE D´OPALE in May 2021 and SALAMANCA in November 2021, offset by vessels sold in 2021.

In October 2022, a contract to sell the ropax vessel CONNEMARA was signed (buyer: Bluebridge Cook Strait Ferries).

Outlook

The fourth quarter has started with volumes in line with pre-pandemic levels.

The high bunker prices, the high inflation and the volatile Swedish krona create uncertainty. 30% of the estimated bunker consumption during the rest of the year is price-guaranteed.

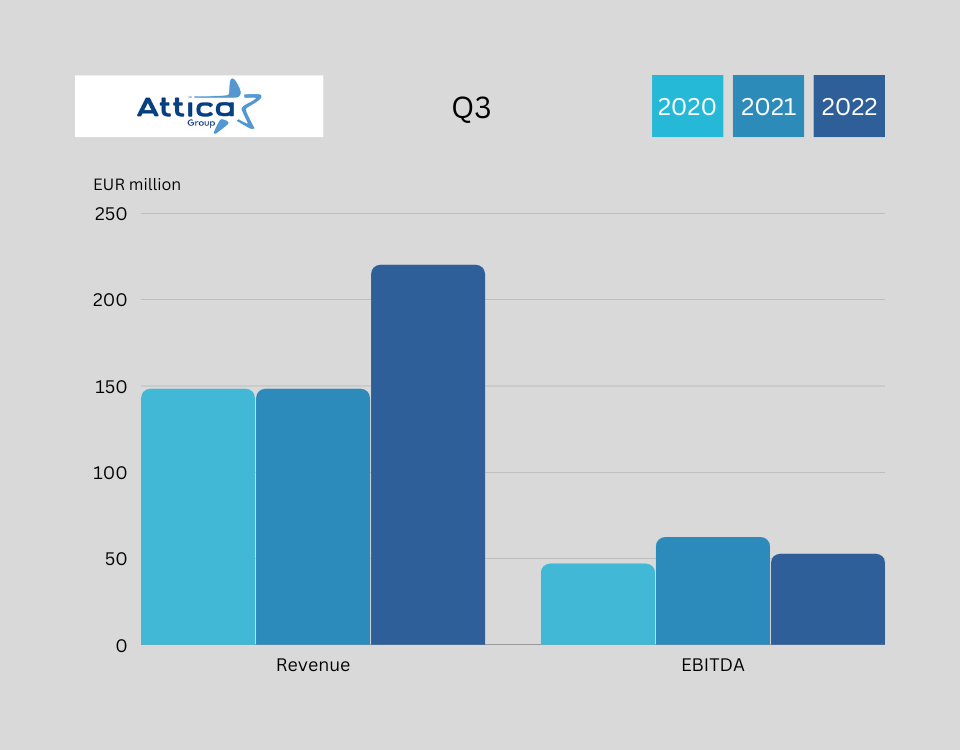

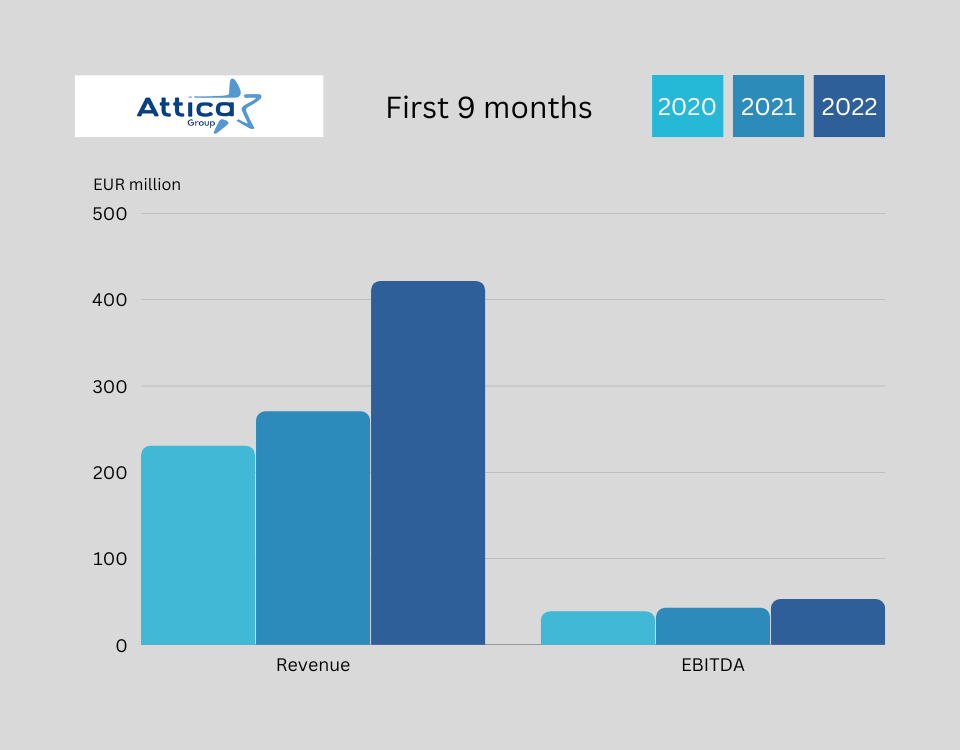

Key Financial Figures (in EUR)

Revenue

Q3= 220.17mln = +48.45%

9M= 421.61mln = +55.86%

EBITDA

Q3= 62.33mln (47.11mln in the corresponding 2021 period)

9M= 52.73mln (42.74mln in the corresponding 2021 periods)

EBIT

Q3= 49.09mln (33.34mln in the corresponding 2021 period)

9M= 14.62mln (4.31mln in the corresponding 2021 period)

Consolidated Profit after taxes

Q3= 60.70mln (profit after taxes of 32.74mln in the corresponding 2021 period)

9M= 30.16mln (loss after taxes of 1.31mln in the corresponding 2021 period)

Outlook

For the forthcoming months of 2022, which constitute months of low traffic, the Group’s traffic volumes are expected to be at pre Covid-19 levels.

Others

The Group holds adequate liquidity with its cash and cash equivalents standing at Euro 75.67mln on 30.09.2022 compared to Euro 97.36mln as at 31.12.2021. Moreover, on 30.09.2022 the Group maintains undrawn credit lines amounting to Euro 15mln.

In October 2022, the Company has entered into bilateral credit facilities with three Greek credit institutions for a total amount of Euro 210mln and tenors from five to seven years, successfully concluding the long-term refinancing of all Group’s credit facilities maturing in 2022- 2023. The above agreements result in the reduction of the average interest rate margin of the Group.

Moreover, ICAP S.A., pursuant to its regular reassessment of the Company, upgraded its credit rating by one (1) notch by assigning it a ΑΑ credit rating (low credit risk zone).

Group revenue increased 64% to DKK 7.2bn driven by the continued recovery in passenger numbers and spending, as well as price increases for freight services to cover rising energy and other costs. Revenue was also increased by the acquisitions of HSF Logistics Group in September 2021 and ICT Logistics in January 2022.

Total EBITDA before special items increased 88% to DKK 1,591m.

The EBITDA for freight ferry and logistics activities increased 28% to DKK 1,036m driven by higher earnings in all business units except for Channel.

Oil price increases were covered by the contractual pass-through clauses for ferry services.

Cost coverage for logistics services improved in Q3 on the back of initiatives taken in previous quarters.

The Q3 EBITDA for passenger activities in the Channel, Baltic Sea, and Passenger business units increased to DKK 569m from DKK 52m in 2021.

The continued recovery in passenger travel improved earnings in all three business units.

Outlook 2022

The outlook for EBITDA before special items is raised to DKK 4.8-5.0bn following a strong Q3 result and steady demand in both freight and passenger markets (previously DKK 4.4-4.8bn, 2021: DKK 3.4bn).

Revenue is expected to grow by around 45% compared to 2021 (previously around 40%). The outlook is detailed on page 10 in the full report.

Q2

H1

Q3

Historically always best quarter of the financial year due to the travel high season.