Key figures:

- Revenue 4,213 DKK m (2,798 in Q2, 2020 and 4,241 in Q2, 2019)

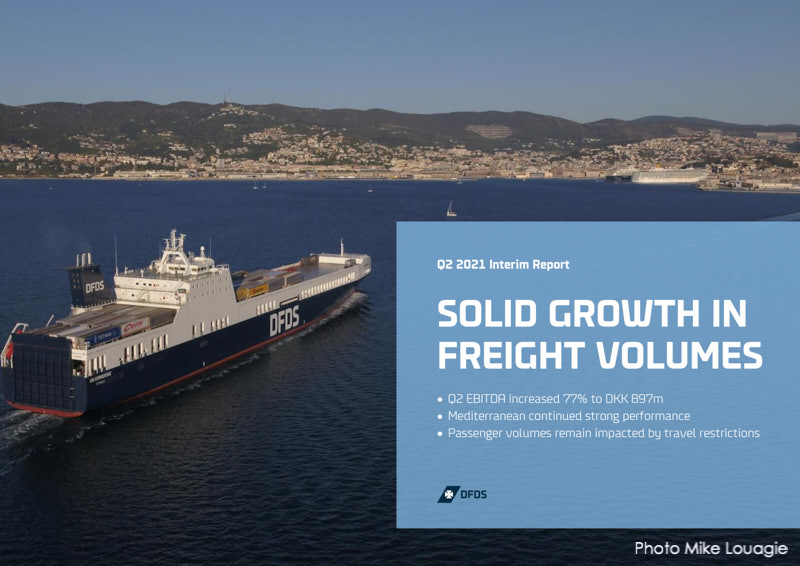

- EBITDA before special items 897 DKK m (507 in Q2, 2020 and 989 in Q2, 2019)

- Profit before tax 328 DKK m (11 in Q2, 2020 and 456 in Q2, 2019)

Highlights

- The growth was driven almost entirely by the freight activities, i.e. freight ferry and logistics.

- Mediterranean continued its strong performance, delivering app. 50% of the Group’s total profit increase.

- Passenger volumes remain impacted by travel restrictions.

Outlook 2021 unchanged

- EBITDA of DKK 3.2-3.6bn

- Revenue growth of 20-25%

- Passenger travel is picking up slower than expected

Market Overview

The European freight market stabilised and growth picked up during Q2 following the Brexit transition that impacted Q1 2021.

The current growth in the freight market, however, exceeds capacity due to shortages of truck drivers and equipment, particularly in the UK. This has led to a rise in haulage costs, longer lead times and less reliable supply chains as well as congestion in some ports. The market imbalance is expected to continue in Q3.

The UK will phase in full import border controls by 1 January 2022, including pre-notification requirements for products of animal origin by 1 October 2021.

Trade between the EU and Turkey continued to grow as the depreciation of the Turkish Lira, continued to benefit Turkish exports. The Turkish economy is expected to continue to grow, primarily driven by the export sector.

Remark

The Dover-Calais space charter agreement with P&O Ferries is expected to become operational around 1 October 2021. It will result in shorter waiting times for truck drivers.

To access the full report, click on the image below: