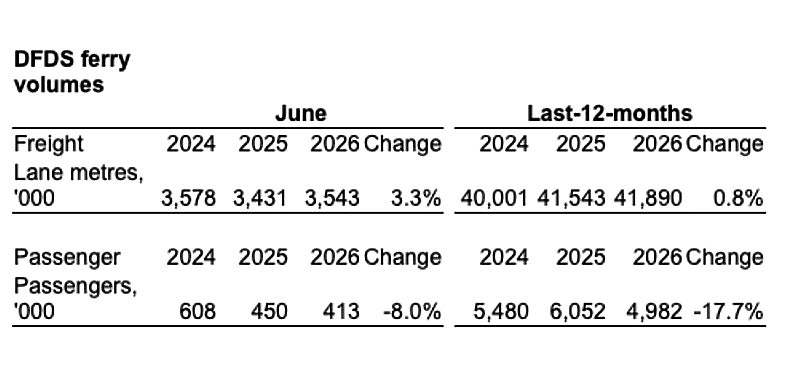

DFDS reported total ferry freight volumes of 3.5 million lane metres in June 2026, an increase of 3.3% compared with June 2025.

Growth was driven by stronger performances in the North Sea, Baltic Sea and Strait of Gibraltar networks. North Sea volumes benefited from higher traffic on most routes and a favourable comparison with June 2025, when a national strike in Sweden impacted volumes. In the Mediterranean, overall freight volumes were lower due to reduced capacity on certain routes, although growth continued on services to Egypt and Tunisia.

Channel volumes were slightly below the level recorded in June 2025.

Over the last twelve months, DFDS transported 41.9 million lane metres of freight, up 0.8% from 41.5 million lane metres in the previous twelve-month period. Adjusted for route changes, freight volumes decreased by 0.4%.

Passenger volumes declined in June. DFDS carried 413,000 passengers, down 8.0% compared with June 2025. The decrease was mainly attributed to fewer departures and lower traffic volumes on the Strait of Gibraltar routes and the Dover Strait.

For the last twelve months, passenger numbers totalled 5.0 million, a decrease of 17.7% compared with 6.1 million in the previous period. Adjusted for route changes, the decline was 5.3%.